Wayne County property reappraisal update

Staff from the county auditor’s office met with several Wayne County Farm Bureau board trustees earlier this spring to give an update on the state-mandated 2026 reappraisal.

Read MoreOhio Farm Bureau is continuing to work multiple channels to address concerns around CAUV – particularly the issue of values spiking significantly. This article was updated in August 2025.

You’ve got CAUV questions, we’ve got answers. In counties undergoing a 2025 revaluation, CAUV values are likely to increase on average 50% from their 2022 level, the last time these counties had a revaluation. Because CAUV is determined by soil type, it is possible that individual soil values may increase more or less than the average rate of increase. CAUV values also increased substantially for counties revalued in 2023 and 2024 as well.

Under the Current Agricultural Use Valuation (CAUV) program, farmland is taxed at a rate that reflects its value for agricultural purposes instead of its value as development property. Recent development like housing, solar farms, or large-scale economic development projects will affect market values of homes and buildings, but it does not impact CAUV values in any way.

[back to top]

The increase in values has largely occurred due to sustained high crop prices over the historical data period of 7 years. Keep in mind that CAUV values are based on the farm economy. In the recent past, we have seen high crop prices – even record prices – that have stayed fairly consistent over the years. The calculation considers seven years of historical crop prices, and while we have seem some drop in crop prices more recently, that historical average is still on the higher side. Because the calculation considers net income, production costs are also an important part of the calculation that lowers the income side of the calculation. While production costs have also increased, they largely increased only in the last year or two. Prior to that, costs were fairly stagnant or saw more incremental increases, particularly compared to crop prices. The CAUV calculation is designed to follow the farm economy, and as the farm economy has been fairly strong in recent years, we have seen the CAUV values respond with increases. For example, in 2011 when we began seeing major increases in CAUV, the highest crop price for corn in the formula was $3.95, today the lowest crop price for corn in the formula is $3.74 per bushel, while the highest price is $6.45 per bushel.

[back to top]

The reform in 2017 was focused upon the non-agricultural factors that were impacting the formula at that time. These factors were largely present in the capitalization rate used in the formula. The capitalization rate is essentially a measure of a good investment, and lower capitalization rates typically mean that the property’s value is higher. Previously when calculating the capitalization rate, the formula took into account interest rates that were wholly unrelated to the farm economy. Those interest rates, particularly in the wake of the 2008 recession, created a significant impact to the CAUV formula through the capitalization rate. This outsized impact of the capitalization rate did not allow the formula to appropriately respond to the drops in crop prices that occurred during that same time frame. Those issues were addressed with reform, and the capitalization rate has stayed fairly consistent since that time. For example, the capitalization rate in 2014, when CAUV values reached their peak, was 6.2%, while the current capitalization rate is 8.4%.

Ohio Farm Bureau secured significant reforms with the Tax Department in 2015 and combined with OFBF’s 2017 legislative reform these actions not only created a more accurate formula, but resulted in the formula better responding to the farm economy, and provided significant savings to CAUV landowners. Most landowners saw an average 30% reduction in value in their first revaluation after reform occurred, and many saw similar reductions in the second revaluation. While the variability of soil values and tax rates makes it hard to pinpoint the savings that resulted from reform, it’s no stretch to say that hundreds of millions of dollars were saved across the state due to CAUV reform.

It is very important to remember that the increase in CAUV value is generally not the same as the increase in your tax bill. CAUV value is one component of your tax bill, but the other important part of that tax bill is the local millage rate of taxation. Ohio’s property taxes require rates to be adjusted to limit how much money is collected for nearly every levy present on your tax bill. This means that often as values increase in a taxing district, the millage rate for those levies will decrease as well. (Note that this does not apply to the first 10 mills on your tax bill, which are authorized by the Ohio Constitution nor millage for schools that are at the 20 mill floor.). While CAUV soil values are determined by the Department of Tax, your millage rate is controlled locally. And, millage rates can vary significantly from one taxing jurisdiction to another.

[back to top]

Typically, county auditors are able to give a better idea of millage rates and tax estimates toward the end of the year.

[back to top]

Individual CAUV land values will vary because they are a unique value to your farm based on the soil types present on your land. Also, keep in mind that we are talking only about CAUV value, and CAUV value only applies to your farm ground. Houses, homesites, and buildings are all valued at market value and are not part of CAUV. Your total property value is going to be a combination of the values of all the components of your property. Residential property values, in general, have also increased significantly across the state. The value statement you receive may or may not break out the different components of your property and their individual value, or it may not specify your market value of farm ground versus the CAUV value of your farm ground. Your county auditor can assist you with that information.

[back to top]

Yes. Despite increases in CAUV, the program still saves significantly on most farmers’ tax bills. Even when CAUV values reached their peak in 2014, CAUV value was on average about 50% of actual market value – representing about the same savings in property taxes on average. The CAUV soil value of Miami Silt Loam in 2025 is set to be $2390 per acre; this is a mid-range productivity soil and the most prevalent soil in the state that is used as a sample soil by the Tax Department. Compare this to the average USDA value of farm ground in Ohio which is currently over $8,700 per acre.

[back to top]

As a result of the 2017 reforms, there is an option to help lower your CAUV value if you are using conservation measures on your farm. Land that is used for federal conservation programs or for private conservation practices that abate soil erosion can be certified with the auditor and valued at the CAUV minimum value of $230/acre. This can be a significant savings, particularly if you have highly productive soils in the areas you are using for conservation. Those programs or practices must stay in place for three years, or there will be a penalty required for their removal. This is not limited to federal conservation programs or H2Ohio funded conservation measures, but can also include privately installed measures that abate soil erosion. Privately installed measures will be limited to 25% of your total CAUV acreage. This important provision resulting from OFBF’s 2017 reform helps to ensure landowners are not penalized by tax policy for installing conservation measures that benefit both their farm and the larger environment.

As to the market values that apply to your house and buildings, if you believe those values are incorrect, property owners can go through the Board of Revision process to appeal. The auditor can assist you in that process. While there is nothing in the law that prevents CAUV values from being appealed through the Board of Revision, these appeals are often less common since CAUV values are done via calculation at the state Department of Taxation level and not performed by your county auditor.

Ohio Farm Bureau is continuing to work multiple channels to address concerns around CAUV – particularly the issue of values spiking significantly. Constitutional limitations do pose an issue for addressing this with only CAUV values – meaning that it may take a larger property tax overhaul to address that problem specifically. We have continued to raise the specific CAUV issues with the Department of Tax directly, and to review the formula for any needed improvements. These discussions resulted in the major updates to woodland values discussed below. In the 2023 state budget, the legislature created a Joint Committee to review property taxation that worked throughout 2024. Ohio Farm Bureau was invited to testify by the committee, and provided background information on CAUV as well as advocated for addressing the volatility in the CAUV program. The legislature and the Governor have continued to look towards broader property tax reform, and OFBF is remaining engaged as it progresses. The property tax system is complicated, and making changes can sometimes have unintended consequences, particularly considering CAUV’s very unique part of the property tax structure. We will continue to work with property tax reform proposals both relative to the concerns of the costs of property taxes, and to ensure CAUV is not harmed by any proposal.

In 2016, Ohio Farm Bureau’s advocacy resulted in an increase of woodland deductions which are used to calculate woodland values. However, OFBF and the Ohio Forestry Association continued to advocate to the Tax Department that these woodland deductions needed further update. Ohio Farm Bureau also advocated in the courts for woodland owners as they challenged the woodland deductions. In 2024, the Department has announced it will further update the woodland deductions beginning in the 2024 reappraisal year. This places nearly all woodland soil values at or near the minimum value of $230/acre for any revaluations in 2024, a trend that continued in 2025 revaluations. Note that about half of woodland soils were at the minimum value prior to this, however, this will significantly impact higher productivity soils valued as woodland. We are also working with our advocacy partners and the Department of Tax to consider how these deductions can be updated regularly to ensure woodland values remain accurate.

Staff from the county auditor’s office met with several Wayne County Farm Bureau board trustees earlier this spring to give an update on the state-mandated 2026 reappraisal.

Read More

Four property tax reform bills were signed into Ohio law at the end of 2025. Ohio Farm Bureau Associate General Counsel Leah Curtis breaks down the bills and what the changes mean for Ohioans.

Read More

OFBF annual meeting delegates will discuss how or if current Farm Bureau policy should be modified in light of various property tax proposals.

Read More

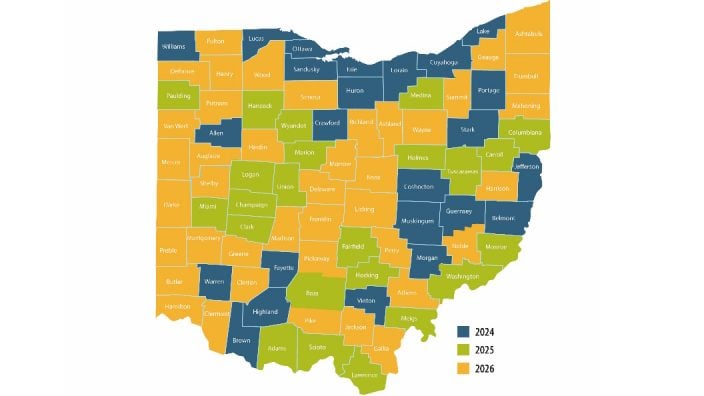

In 2025, about 21 counties are going through a reappraisal or update, and because Ohioans pay taxes one year behind, they will see new property tax bills in January 2026.

Read More

Overall, proper care, maintenance and communication are all essential parts of the process when it comes to trees.

Read More

This will apply to the 23 counties on the revaluation cycle in 2025, who will see updated values and tax bills in January 2026.

Read More‘We never stop pushing to ensure farmland taxation is fair and reflects the realities of agriculture.’ ~ Mandy Orahood

Read More

In this recording, learn about the recent increases in Ohio CAUV values, gather information to help you understand the property tax system, and get an update on legislative action.

Read More

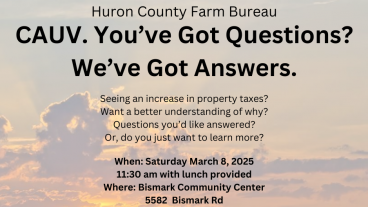

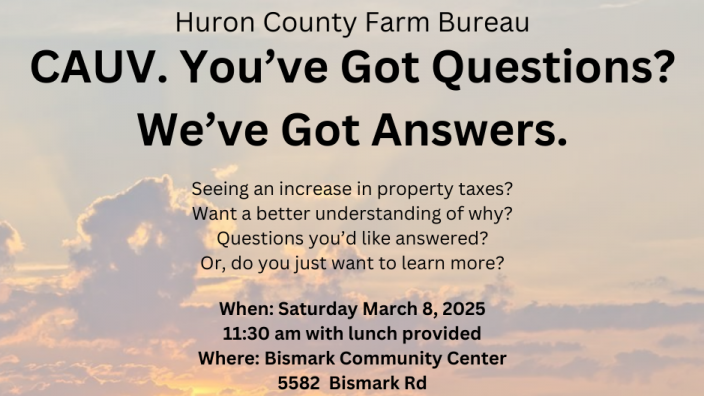

Join us for an informative session March 8. Experts will explain recent changes, answer your questions, and help you better understand how CAUV impacts you.

Read More

Lorain County Farm Bureau hosted a CAUV meeting Jan. 30, 2025 at LCCC Wellington Center presented by the Lorain County Auditor’s Office and Lorain County Farm Bureau.

Read More